December 13, 2021

Labor Inflation: Exported

Baltic Dry Index:

Unyielding debt limits:

This is going to be a longer blog than usual; we are going to break it up into two parts. Further, while we are writing about China, we are going to tie it into our main thesis regarding money printing by central banks.

(The money printing that builds upon a central bank’s balance sheet we call Quantitative Easing. The reduction of this balance sheet we call Quantitative Tightening.)

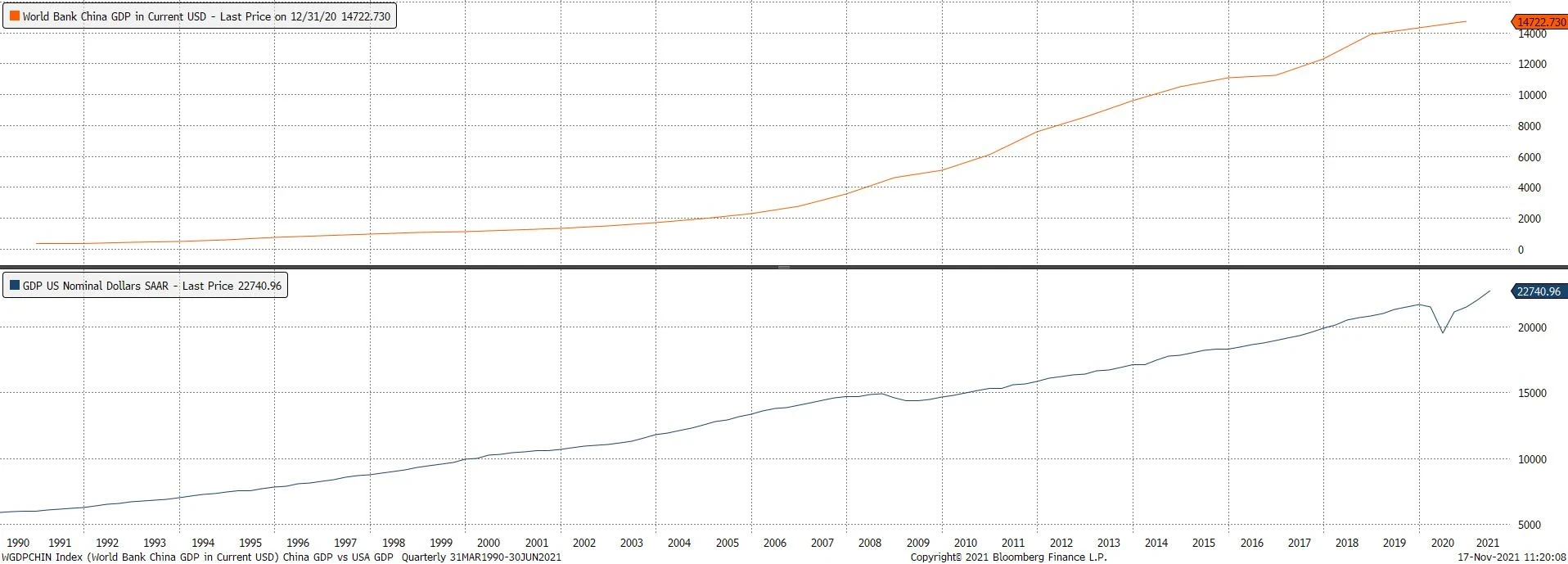

In the last 30 years, China’s economy measured by GDP has been explosive. It is now the second-largest economy in the world. China has the world’s largest population with approximately 1.4 billion people.

There is a lot of rhetoric that seems to imply China’s growth was at our expense, which we feel is unfounded. The USA, for the last 30 years, has had robust economic growth as well. China and the USA have become strategic economic partners, and we believe will continue for years to come. GDP in the USA is north of $23 trillion, and China is north of $15 trillion.

USA and China GDP:

A common focus throughout our blogs has been around three key areas: inflation, interest rates, and the money printing by the Federal Reserve Bank. All three of these factors are relevant to our relationship with China, and China has been strategic in helping the USA moderate inflation as measured by labor inflation. We do not want to understate the importance of having China manufacture so much for us. Exporting jobs or labor has been essential if not necessary for the US in managing inflation while enjoying our economic growth. Historically, inflation is measured mainly by two key components: labor inflation (wage inflation) and commodity inflation (crude oil).

In other words, the USA has been able to export much of its manufacturing labor inflation by having things made in other countries with more favorable labor costs as well as currency exchange. China fits both factors.

How awesome are the results of exporting labor inflation? It has kept the cost of goods lower for the consumer in the US, helped the profit margins of many US companies, and helped China grow at an amazing clip. Most Americans are aware of goods imported from China for one reason or another. Today we are painfully aware as we wait for our orders to be unloaded at the overloaded ports. It seems, every day someone is talking about the large number of ships anchored waiting their turn to unload.

There are consequences to manufacturing in another country. We would assume companies and politicians considered those consequences in their analysis; yet, after reading many news headlines, we wonder.

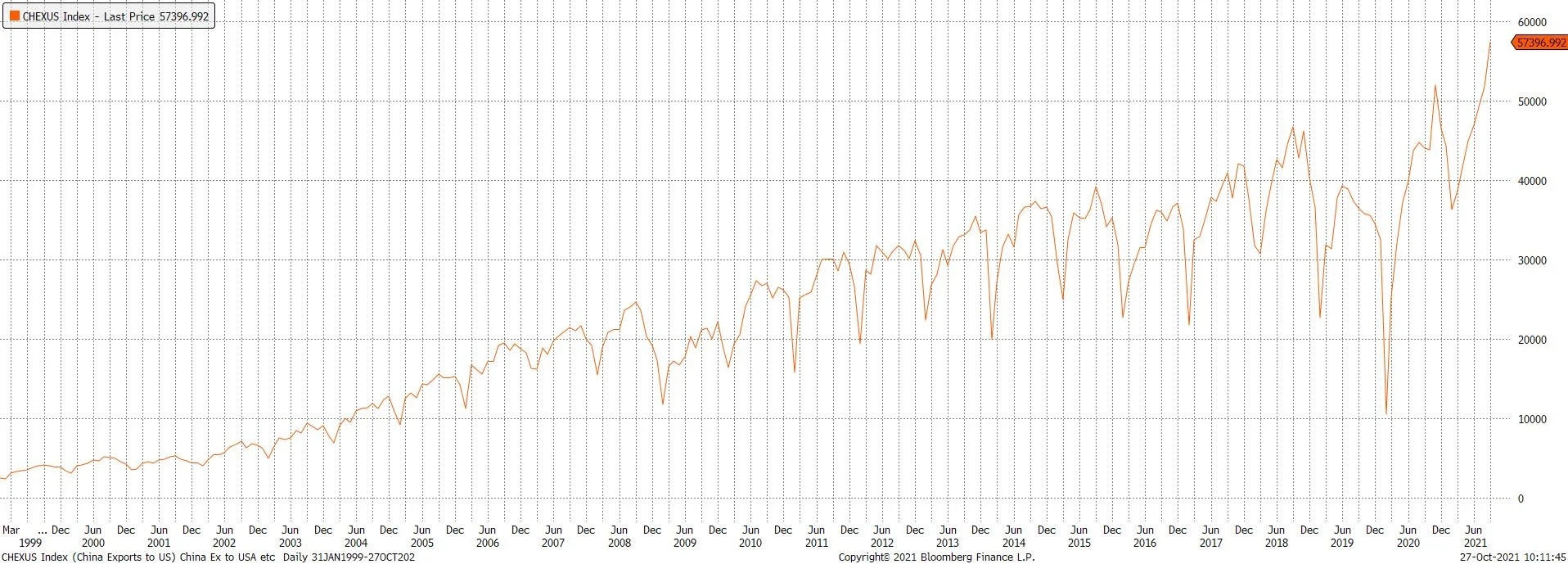

China Exports to the USA:

We asked a handful of people if the USA is importing less from China, the same, or more. Most guessed it is less. You might be surprised; we are importing more than ever. We have imported about $537 billion so far this year.

Please see chart:

The chart below shows the growth of our exports to China. Currently, we have exported about $109 billion to China:

China Imports from the USA:

Yes, we have imported less from China than they imported from us; however, you must put into the equation the exportation of labor inflation. It is abstract and hard to quantify. So, we will repeat ourselves:

By exporting our manufacturing to China with a much lower hourly wage cost, combined with a currency with a favorable exchange rate, such as China, we export our inflation and bring in labor at a deflated cost. This requires as many of the variables to be as fixed as possible. So, if China pegs their currency to our dollar this is not nefarious currency manipulation.

If China had things manufactured in the USA, then they would be importing inflation, which would make no sense. It makes sense for China to import crude oil and food items which are not readily available to them. Likewise, it makes sense for us to import China’s labor costs, thereby importing deflated labor.

One cost that is not fixed is the time it takes to ship, unload, and transport items to their destination. Of course, there is no surprise the cost of transportation is going up.

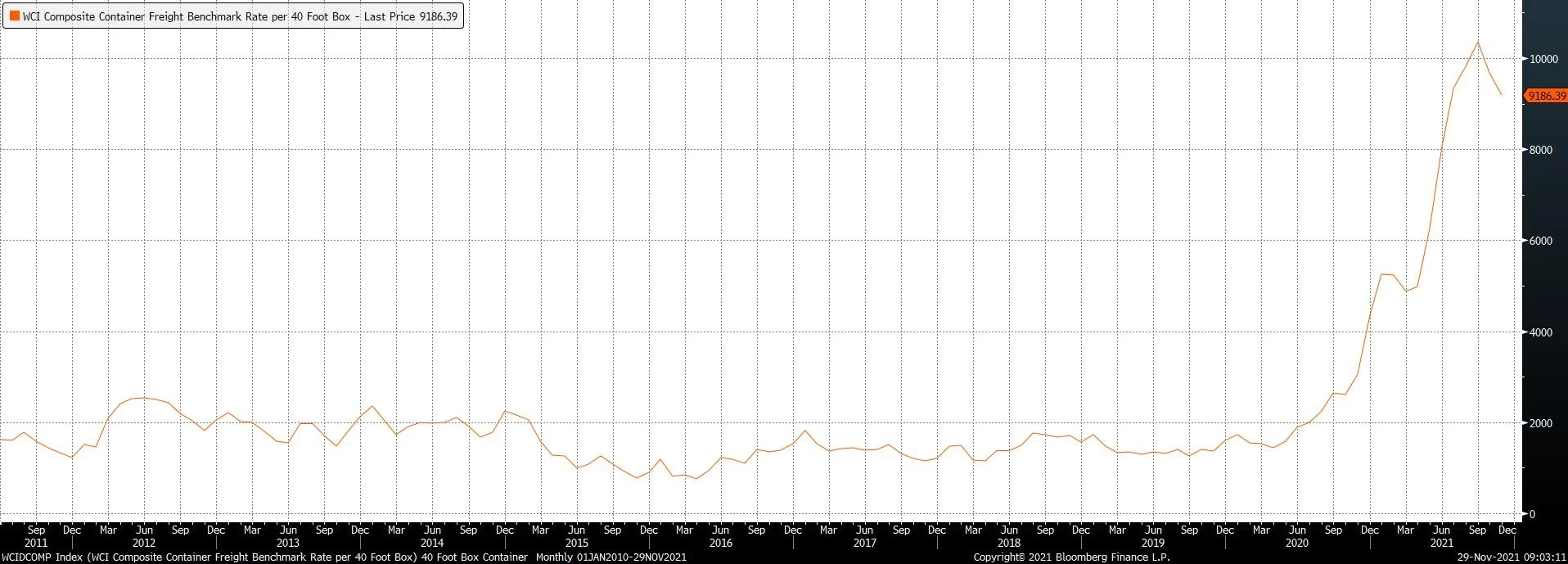

Everyone knows inflation is permeating many aspects of our financial lives. Shipping costs are a great example. Let’s look at a box container cost.

Below is a graph of the cost of shipping a forty-foot container:

Now let us look at the global cost of shipping. There is an index called the Baltic Dry Index. There is no surprise the charts look similar.

Please see chart:

Clearly, the cost of packaging and shipping has increased dramatically. If these costs are transitory, like the spike in lumber prices, as we argued in our last lumber blog, then there may not be too much to worry about. Why worry about inflation? We are concerned because it has the potential to derail the economy. Fighting inflation is one of the functions of the Federal Reserve. However, we have argued since they are all in on the money printing stimulus, they have all but forfeited their ability to fight inflation. We have made several observations regarding the consequences of their policy, specifically Quantitative Easing (QE).

We have been writing about QE in all our blogs. We have argued that keeping inflation in check has allowed our Federal Reserve bank to do Quantitative Easing and keep the prime rate near zero. We always want to remind our readers that QE is a Faustian deal: once you make that deal, once you go down that path, there is no going back. Further, we have argued a consequence of money printing by the Fed is the difficulty of fighting inflation.

Let us revisit the USA financial crisis of 2008-2009 when the money printing (QE) by the Fed began. We had a housing price bubble and many financial companies had too much debt related to the real estate market on their balance sheet, which blew up along with the USA real estate market. As a side note, I was told recently, “real estate will never have a severe correction again.” Has the boom-and-bust cycle ended? We highly doubt this!

Today China is in the news a lot as they are having their own financial difficulty regarding their real estate market. We will write more about this in our second China blog. For now, are we concerned that their financial system will be destroyed like ours was, we do not think so. While we take any financial disruption seriously, we believe China has the leadership and financial health to work through this successfully. However, we do think it could be a harbinger of real estate around the globe peaking in value and the beginning of a correction.

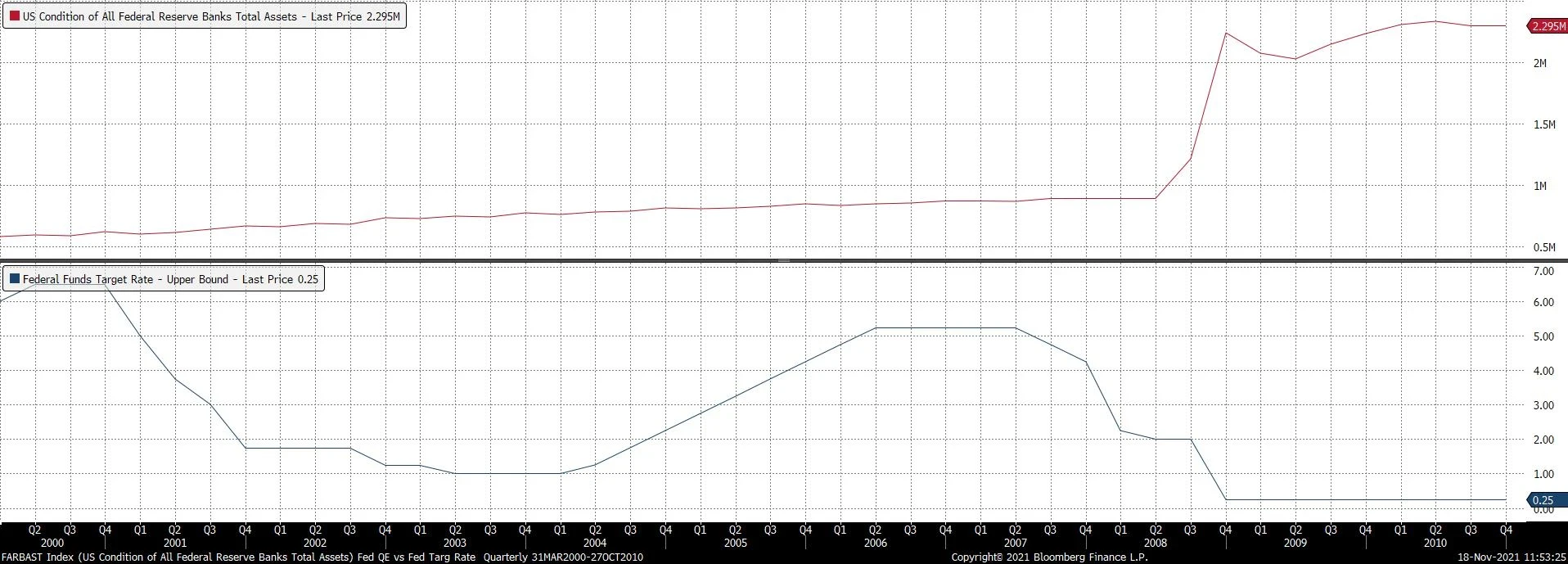

Our housing bubble was preceded by a dot-com bubble, which popped around 2000-2001. Again, the Fed lowered the prime rate aggressively. What followed was an expansion of credit and the housing market and crude oil market having several years of price increases creating a bubble of their own. Of course, what followed was a series of rate hikes from 2004-2006 to cool things off. However, there was a severe housing bubble developing and it popped in 2008. What followed was a retracement of rate hikes to a level of 0.25 percent, and the Federal Reserve balance sheet began its assent- a new cool tool to add additional stimulus called Quantitative Easing.

Please see the chart: the top line is the Federal Reserve balance sheet. The bottom blue line is the Fed target rate.

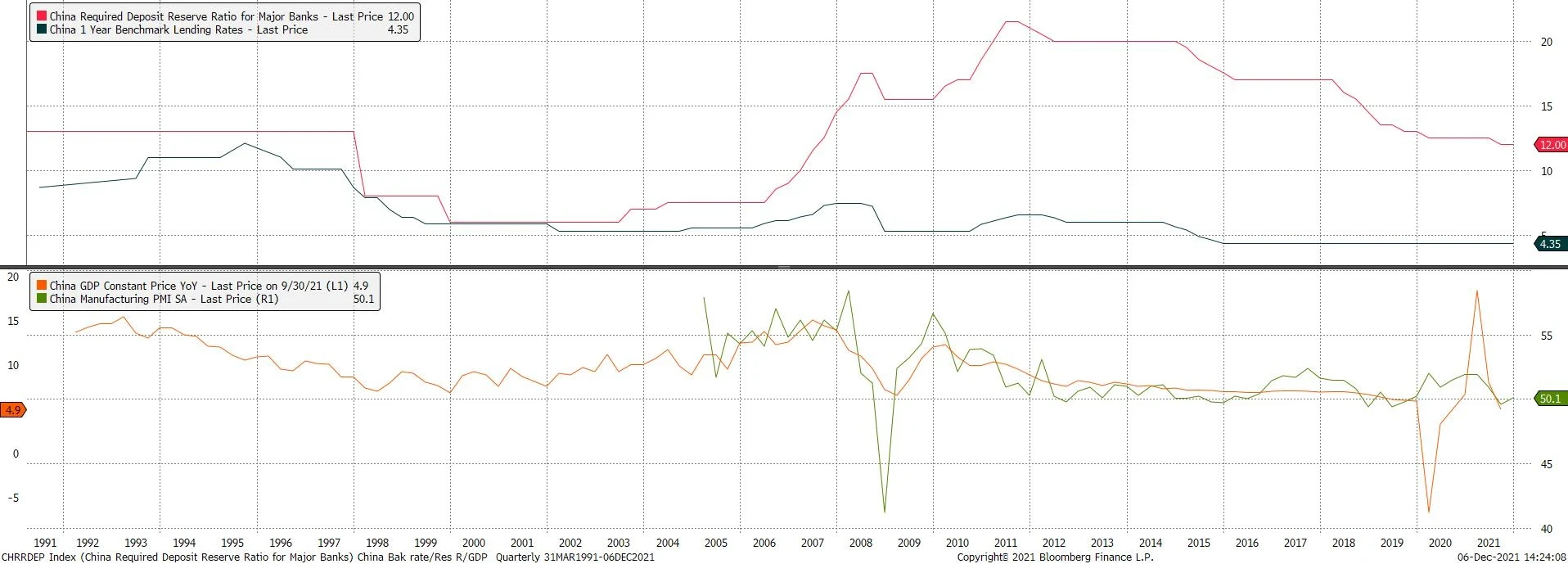

Now let us go back to look at what was happening in China around 2008. Just like in the USA before 2008, China was raising its prime rates and bank reserve requirements to slow down its economy.

Their GDP in 2007 was about 15%. Their prime rate was raised to over 7% and their bank reserve requirement to over 17%.

See chart: the top red line: bank reserve requirement; top blue line: the prime rate; bottom orange line: GDP; bottom green line: PMI.

China was forced to lower its prime rate and bank reserve requirement as the USA faced systemic failure of its banking system.

There are other similarities between now and 2008. Specifically, shipping rates as indicated by the Baltic Dry Index (BDI). We mentioned this index above. (We are going to tie a lot of concepts in our previous blogs together in this one.) The BDI was once used as an indicator of a strong or weak economy; however, as the index went sidewise since 2010 it seemed to have lost its value as a barometer. The recent spike in the index might be good news depending on one’s perspective. We see it as a double-edged sword. On the one hand, clearly, there is a lot of demand for goods, and on the other, robust inflation.

Okay, so what’s the big deal? Well, here is why it is potentially a big deal.

Take a longer view of the Baltic Dry Index. You can see that the level today is about where it was in 2004-2006, then it climbed to a new high in 2007, which was the beginning of the great financial crisis. The Fed had done a series of rate hikes to fight inflation, but there is a lag before it is felt in the economy.

Please see chart:

The current level has not been this high since 2004. As we mentioned, the Fed was raising rates starting in 2003 to slow down the economy; they kept raising rates and the peril of a popped housing market was the consequence. We have argued that inflation, specifically crude oil inflation, is the Achilles heel to money printing by central banks. Labor costs can be exported to other countries with more favorable labor costs. Now we have 3 components of inflation going higher- labor, oil, and transportation.

Obviously, we are very curious how this plays out over the next few years. On the one hand, we can see the index climbing and forcing the Fed to raise rates and begin to not only slow down monthly purchases but also reduce their balance sheet. This would bring a lot of volatility to risk assets, not only the stock market as it did in 2018, but also to the real estate market. On the other hand, if the spike in the Baltic Dry Index is transitory, and comes back down, then we could have smooth sailing. If it doubles again as it did between 2004 and 2007 then we could have a real problem.

This is reminiscent of our lumber blog. In our last blog, we addressed the high cost of lumber. Not long after we posted that blog, the cost of lumber retreated over $1000 per 1000 board feet. The Baltic Dry Index is more complex.

DISCLOSURE:

SPX INDEX: S&P 500, or simply the S&P, is a stock market index that measures the stock performance of 500 large companies listed on stock exchanges in the United States. It is one of the most commonly followed equity indices, and many consider it to be one of the best representations of the U.S. stock market.

GDP CURY INDEX: Gross Domestic Product (GDP) is the monetary value of all finished goods and services made within a country during a specific period. GDP provides an economic snapshot of a country, used to estimate the size of an economy and growth rate. GDP can be calculated in three ways, using expenditures, production, or incomes. Apr 29, 2020, Investopedia

China GDP:

GDP at purchaser's prices is the sum of gross value added by all resident producers in the economy plus any product taxes and minus any subsidies not included in the value of the products. It is calculated without making deductions for depreciation of fabricated assets or for depletion and degradation of natural resources. Data are in current U.S. dollars. Dollar figures for GDP are converted from domestic currencies using single-year official exchange rates. For a few countries where the official exchange rate does not reflect the rate effectively applied to actual foreign exchange transactions, an alternative conversion factor is used. World Bank national accounts data, and OECD National Accounts data files. Data is updated with a 1-2 year lag due to the large amount of data processed by the World Bank. Yearly data is therefore available around September of the current year for the previous year. Bloomberg.

Quantitative easing (QE) is a monetary policy whereby a central bank buys government bonds or other financial assets in order to inject money into the economy to expand economic activity. Wikipedia

The Fed Balance Sheet

FEDL01 Index:

Until March 1, 2016, the daily effective federal funds rate was calculated by the New York Fed as a volume-weighted mean of overnight rates on trades arranged by major brokers. As of March 1, 2016, the New York Fed is reporting the daily volume-weighted median value of trades provided by the brokers. All rates are subject to revision by the New York Fed. Bloomberg

FEDL01: is a spliced series of the mean-based calculated values of the effective rate (prior to March 1, 2016) and the median-based calculated values of the effective rate (from March 1, 2016).

4.1 report: which provides a consolidated statement of the condition of all the Federal Reserve banks, in terms of their assets and liabilities. ... It lists all assets and liabilities, providing a consolidated statement of the condition of all 12 regional Federal Reserve Banks.

May 11, 2020, Investopedia

In the United States, the federal funds rate is the interest rate at which depository institutions lend reserve balances to other depository institutions overnight on an uncollateralized basis. Reserve balances are amounts held at the Federal Reserve to maintain depository institutions' reserve requirements. Wikipedia

The Baltic Dry Index (BDI) is an index of average prices paid for the transport of dry bulk materials across more than 20 routes. The BDI is often viewed as a leading indicator of economic activity because changes in the index reflect supply and demand for important materials used in manufacturing. Jan 26, 2021, Bloomberg.

The tickers under ALLX CHRR <GO> log the required reserve ratio (and its cut). The tickers will only capture cuts that are enjoyed by all banks.

From September 2017, PBoC started to conduct "targeted Required Reserve Ratio cuts" to support medium and small-sized enterprises. Such rate cuts would only be given to inclusive banks or institutions that satisfy certain criteria. This information is bank-specific and usually not publicly released on regular basis.

Given this, RRR tickers can be different from the snapshot that pboc provided on June 12, 2020, which displayed the optimized rates for large, medium, and small banks respectively. Bloomberg.

These are the Best Lending Rates for various tenors determined by People's Bank of China.

PBOC announced Loan Prime Rate in Aug 2019 as benchmark lending rate. Bloomberg.

The views stated in this letter are not necessarily the opinion of Cetera Advisor Networks LLC and should not be construed directly or indirectly as an offer to buy or sell any securities mentioned herein. Due to volatility within the markets mentioned, opinions are subject to change with or without notice. Information is based on sources believed to be reliable; however, their accuracy or completeness cannot be guaranteed. Past performance does not guarantee future results. Investors cannot invest directly in indexes. The performance of any index is not indicative of the performance of any investment and does not consider the effects of inflation and the fees and expenses associated with investing.

Investment advisor representative of, and securities and investment advisory services offered through Cetera Advisor Networks LLC, member FINRA/SIPC, a broker/dealer, and Registered Investment Advisor. Cetera is under separate ownership from any other named entity. Investment advisory services are also offered through Fulcrum Wealth Advisors, LLC. Fulcrum Wealth Advisors LLC is a registered investment advisor in the State of Washington. / IRS Circular 230 Disclosure: Fulcrum Wealth Advisors does not provide legal, tax, or accounting advice. Any statement contained in this communication (including any attachments) concerning U.S. tax matters is not intended or written to be used, and cannot be used, for the purpose of avoiding penalties imposed on the relevant taxpayer. Clients of Fulcrum Wealth Advisors should obtain their own independent tax advice based on their particular circumstances.

All charts courtesy of Bloomberg Finance L.P.

Fulcrum Wealth Advisors, LLC, 10940 NE 33RD Place, Suite #210 Bellevue, WA 98004